About one method of finding expected incomes in HM-queueing network with positive customers and signals

Mikhail Matalytski

Journal of Applied Mathematics and Computational Mechanics |

Download Full Text |

ABOUT ONE METHOD OF FINDING EXPECTED INCOMES IN HM-QUEUEING NETWORK WITH POSITIVE CUSTOMERS AND SIGNALS

Mikhail Matalytski

Institute of Mathematics, Czestochowa

University of Technology

Częstochowa, Poland

m.matalytski@gmail.com

Abstract. In the paper an open Markov HM(Howard-Matalytski)-Queueing Network (QN) with incomes, positive customers and signals (G(Gelenbe)-QN with signals) is investigated. The case is researched, when incomes from the transitions between the states of the network are random variables (RV) with given mean values. In the main part of the paper a description is given of G-network with signals and incomes, all kinds of transition probabilities and incomes from the transitions between the states of the network. The method of finding expected incomes of the researched network was proposed, which is based on using of found approximate and exact expressions for the mean values of random incomes. The variances of incomes of queueing systems (QS) was also found. A calculation example, which illustrates the differences of expected incomes of HM-networks with negative customers and QN without them and also with signals, has been given. The practical significance of these results consist of that they can be used at forecasting incomes in computer systems and networks (CSN) taking into account virus penetration into it and also at load control in such networks.

Keywords: HM-queueing network, positive and negative customers, signals, expected incomes, transient regime

1. Introduction

For the first time Markov nets with positive customers and signals were introduced and investigated at the non-stationary behavior by E. Gelenbe, see [1]. The action of the signal consists of instantaneous movement of positive customers of this system to some other network system. The signal may work as a trigger, which doesn’t destroy the customers, but only moves them instantly with a given probability of a given system to another network system.

In developing models of computer viruses we can use negative customers. And for load control in the network can be inputted signals (triggers). When viruses penetrate into computers in the information system, it suffers costs or losses due to the loss of information or CSN distortion. The accounting of the losses in CSN can be realized with the help of a Markov QN model with incomes (HM-networks), positive and negative customers and signals.

In this paper, an open Markov HM-network with positive and negative customers, signals, when the incomes from the transitions between the states of the network are random variables (RV) with time-dependent customer servicing in the systems has been carried out. The expressions for the variances of incomes of queueing systems (QS) was also obtained.

A description of the network is given in [2, 3].

Signal, coming in an empty

system ![]() (in which there are no positive

customers), does not have any impact

on the network and immediately disappeared from it.

Otherwise, if the system

(in which there are no positive

customers), does not have any impact

on the network and immediately disappeared from it.

Otherwise, if the system ![]() is not empty, when it receives a signal, the following events may

occur: incoming signal instantly moves the positive customer from the system

is not empty, when it receives a signal, the following events may

occur: incoming signal instantly moves the positive customer from the system ![]() into the system

into the system

![]() with probability

with probability ![]() in this case, signal is referred

to as a trigger; or with

probability

in this case, signal is referred

to as a trigger; or with

probability ![]() signal is triggered by a

negative customer and destroys in QS

signal is triggered by a

negative customer and destroys in QS ![]() positive customer. The state

of the network meaning the vector

positive customer. The state

of the network meaning the vector ![]() where

where ![]() - the number of customers

at the moment

of time

- the number of customers

at the moment

of time ![]() at the system

at the system ![]() ,

, ![]() .

.

2. Description of incomes from the transitions between the states of the network

Let ![]() -

time of customers service in the system

-

time of customers service in the system ![]() with

the distribution function (DF)

with

the distribution function (DF) ![]() ,

, ![]() . Consider the dynamics of income

changes of

a network system

. Consider the dynamics of income

changes of

a network system ![]() ,

, ![]() . Let at the initial moment of time the income of

this QS be equal to

. Let at the initial moment of time the income of

this QS be equal to ![]() . We are interested

in income

. We are interested

in income ![]() at time t. The income of its QS

at moment time

at time t. The income of its QS

at moment time ![]() can be represented in the

form

can be represented in the

form ![]() , where

, where ![]() -

income changes of the system

-

income changes of the system ![]() at the time interval

at the time interval

![]() ,

, ![]() .

.

To find the income of the system ![]() we write the conditional probabilities

of the events that may occur during

we write the conditional probabilities

of the events that may occur during ![]() . The following cases

are possible:

. The following cases

are possible:

1) with

probability ![]() to the system

to the system ![]() from the external environment

a positive customer will arrive, which will bring an income in the amount of

from the external environment

a positive customer will arrive, which will bring an income in the amount of ![]() , where

, where ![]() - RV with expectation (E) of

which equals

- RV with expectation (E) of

which equals ![]() ,

, ![]() ;

;

2) with probability ![]() in the QS

in the QS ![]() from the external environment

a signal will arrive, which will bring an income (loss) in the amount of signal

is triggered by a negative customer and destroys in QS

from the external environment

a signal will arrive, which will bring an income (loss) in the amount of signal

is triggered by a negative customer and destroys in QS ![]() positive customer, which will bring a

loss in the amount of

positive customer, which will bring a

loss in the amount of ![]() ,

where

,

where ![]() - RV with E

- RV with E ![]() ,

, ![]() ;

;

3) the incoming

signal instantly moves the positive customer from the system ![]() into the system

into the system ![]() probability

of this event equals

probability

of this event equals ![]()

![]() ,

, ![]() by this transition the income of

by this transition the income of ![]() is reduced by the amount

is reduced by the amount ![]() , and income of

, and income of ![]() is

increased by this amount, where,

is

increased by this amount, where, ![]() - RV with E

- RV with E ![]() ,

, ![]() ;

;

4) with probability ![]() a positive customer will depart from

the network to the external environment, while the total amount of income of QS

a positive customer will depart from

the network to the external environment, while the total amount of income of QS

![]() is reduced by an amount which is equal

to

is reduced by an amount which is equal

to ![]() , where

, where ![]() - RV with E

- RV with E

![]() ,

, ![]() ;

;

5) with probability ![]() a customer from the

system

a customer from the

system ![]() transit to the system

transit to the system ![]() as a signal, if in it there were no

customers, and the income of

as a signal, if in it there were no

customers, and the income of ![]() is reduced by the

amount

is reduced by the

amount ![]() , where

, where ![]() - RV with E

- RV with E

![]() ,

, ![]() ;

;

6) a customer from

the QS ![]() transit to the system

transit to the system ![]() with probability

with probability ![]()

![]() ,

, ![]() by such a transition the income of

system

by such a transition the income of

system ![]() is reduced by the amount

is reduced by the amount ![]() and the income of system

and the income of system ![]() is

increased by this amount,

is

increased by this amount, ![]()

![]() ,

, ![]() ,

, ![]()

7) with probability ![]() positive customer transit from the

system

positive customer transit from the

system ![]() to the system

to the system ![]() , wherein the income of the QS

, wherein the income of the QS ![]() will increase

by the value of

will increase

by the value of ![]() , and the income of

, and the income of ![]() is reduced by this amount,

is reduced by this amount, ![]() ,

, ![]() ,

, ![]()

8) after

finishing servicing of a positive customer in QS ![]() it

is sent to

it

is sent to ![]() as

a signal, which is triggered by a negative customer and destroyed in QS

as

a signal, which is triggered by a negative customer and destroyed in QS ![]() positive customer; the probability of

this event equals

positive customer; the probability of

this event equals ![]() ; wherein the income of the QS

; wherein the income of the QS

![]() will reduce by value

will reduce by value ![]() , and the income of

, and the income of ![]() is reduced also by the amount,

is reduced also by the amount, ![]() ,

, ![]() ,

, ![]()

9) after finishing

servicing of positive customer in QS ![]() , it is sent to

, it is sent to ![]() as

a signal, which instantly moves the

positive customer from the system

as

a signal, which instantly moves the

positive customer from the system ![]() into the system

into the system ![]() the probability of this

event equals

the probability of this

event equals ![]() ,

, ![]() ,

, ![]() ,

, ![]() by such a

transition the income of system

by such a

transition the income of system ![]() and

and ![]() reduced

by the amount

reduced

by the amount ![]() , and income of system

, and income of system ![]() is increased by

this amount respectively, where

is increased by

this amount respectively, where ![]() - RV with

the E

- RV with

the E ![]() ,

, ![]() ,

, ![]()

![]()

10) with probability ![]() on time interval

on time interval ![]() network state will not change;

network state will not change;

11) for every small time interval ![]() system

system

![]() because of customers’ presence

in it increases its income by the amount of

because of customers’ presence

in it increases its income by the amount of ![]() ,

where

,

where ![]() - RV with the E

- RV with the E ![]() ,

, ![]() .

.

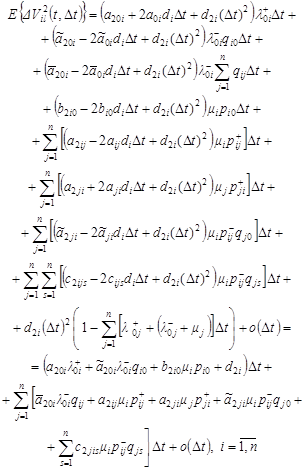

3. Finding the expected incomes of the network systems

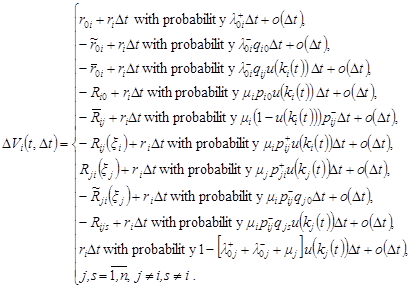

Income changes of the QS ![]() on interval

on interval ![]() can

be written as:

can

be written as:

| (1) |

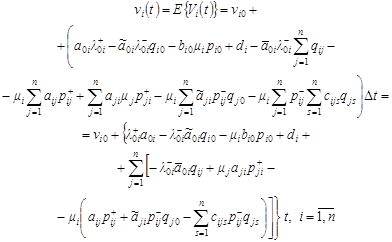

Let us find the expression for the expected

income of the system ![]() in time

in time ![]() suppose, all the network systems

operate under heavy-traffic regime, i.e.

suppose, all the network systems

operate under heavy-traffic regime, i.e. ![]()

![]()

![]() Taking into account (1) for the E

or income changes we can write:

Taking into account (1) for the E

or income changes we can write:

|

Then, similarly as in [3], we obtain

| (2) |

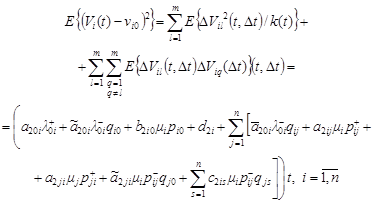

4. Finding variances of the incomes of the network systems

As in

[4], system income ![]() can be presented in form

can be presented in form ![]() , where

, where ![]() - count of partitions of the interval

- count of partitions of the interval ![]() by equal parts,

by equal parts, ![]() ;

;

![]() - income changes i-th

QS on l-th time interval,

- income changes i-th

QS on l-th time interval, ![]() ,

, ![]() . To calculate the variance of the

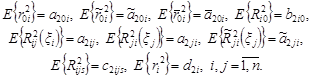

system income in the network, we introduce the following designations:

. To calculate the variance of the

system income in the network, we introduce the following designations:

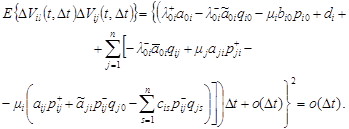

|

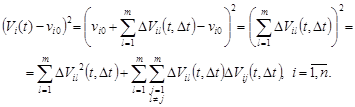

Let us consider the square of the difference ![]()

| (3) |

Let us find the expectations of summands in

the right side of the last equality. For

this we write support equalities considering that RV and functions of RV

![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() pairwise independent from

pairwise independent from ![]() ,

, ![]() . Then

. Then

| (4) |

| (5) |

| (6) |

| (7) |

| (8) |

| (9) |

| (10) |

| (11) |

Considering (4)-(11), we have:

| (12) |

Insofar

as the values ![]() and

and ![]() are independent at

are independent at ![]() using (12)

one can find

using (12)

one can find

| (13) |

Then, further, passing to the limit ![]() from (3),

(12), (13) and also, that

from (3),

(12), (13) and also, that ![]() obtain

obtain

| (14) |

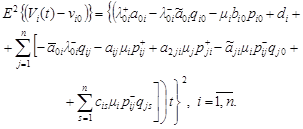

Now let us find an expression for ![]() , using (2):

, using (2):

| (15) |

In this way, the variance of income of i-th QS, considering (14), (15), can be written in the form

| (16) |

5. Numerical example

As is

known (see [5]), relation for the expected income of the system ![]() in the case,

where there are no negative customers in the network and all systems operate in

a heavy-traffic regime, has the form:

in the case,

where there are no negative customers in the network and all systems operate in

a heavy-traffic regime, has the form:

| (17) |

where: ![]() - input rate

of customers;

- input rate

of customers; ![]() - probability of a

customer arriving to the system

- probability of a

customer arriving to the system ![]() ,

, ![]() ,

, ![]() ;

; ![]() - probability that the customer

which finished servicing in i-th QS move to j-th QS,

- probability that the customer

which finished servicing in i-th QS move to j-th QS, ![]() ,

, ![]() ;

; ![]() - probability of the

departure of a customer,

- probability of the

departure of a customer, ![]()

![]() . Relation for the expected income of

the system

. Relation for the expected income of

the system ![]() with negative customers but without

considering input signals, can be written as [6]:

with negative customers but without

considering input signals, can be written as [6]:

| (18) |

Let n = 10; input rates of

positive customers and signals ![]() and

and ![]() respectively equal

respectively equal ![]() ,

, ![]() ,

, ![]() . Service rates of customers

. Service rates of customers ![]() equal

equal ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() . Let

us transition probabilities of positive customers

. Let

us transition probabilities of positive customers ![]() respectively

equal:

respectively

equal: ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() , other equal zero. Probabilities, that

were serviced in

, other equal zero. Probabilities, that

were serviced in ![]() , move to

, move to ![]() as

negative, equal:

as

negative, equal: ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

other equal zero. Departure probabilities equal

,

other equal zero. Departure probabilities equal ![]() ,

, ![]() . Probabilities of a signal

arriving, which are instantly moves the positive customer from the system

. Probabilities of a signal

arriving, which are instantly moves the positive customer from the system ![]() to the system

to the system ![]() respectively equal:

respectively equal: ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

other equal zero. Probabilities that signal is triggered as a negative customer

and destroys

in QS positive customer equal:

,

other equal zero. Probabilities that signal is triggered as a negative customer

and destroys

in QS positive customer equal: ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() .

.

Let us set values for the required

expectations: ![]() ,

, ![]() ,

,

![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ;

; ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ;

; ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ;

; ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ;

; ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ;

; ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

other equal zero.

,

other equal zero.

Expectations

for the random system of incomes has been calculated. Their values have the form: ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ;

; ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() ,

, ![]() .

.

Let us suppose that income at the initial time equals ![]()

![]() .

Consider the length of the time interval of 10 hours,

.

Consider the length of the time interval of 10 hours, ![]() ,

,

![]() . Then using formulas (2), (17), (18)

analytical expressions have been found for the expected system

incomes of the networks.

. Then using formulas (2), (17), (18)

analytical expressions have been found for the expected system

incomes of the networks.

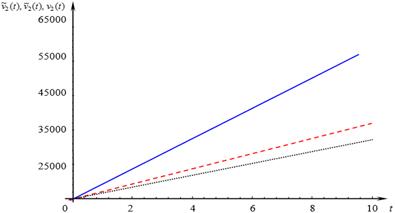

In Figure 1, income changes is shown of the QS ![]() for HM-network with

negative customers and without them, and also with

signals. One can see that

the negative customers reduce

expected income of the system

for HM-network with

negative customers and without them, and also with

signals. One can see that

the negative customers reduce

expected income of the system ![]() Signals inputting also influence the income changes, reducing it.

Signals inputting also influence the income changes, reducing it.

Fig. 1. Income changes of the S2 QS, solid line - a case without negative customers, dashed - a case with negative customers, dotted - taking into account the signals

6. Conclusions

In this paper a method was proposed for finding expected incomes in HM-network systems with positive and negative customers and also with signals. Incomes from the transitions between the states of the network are RV with given mean values. This method is based on the using of found approximate and exact expressions for the mean values of the random incomes. An example was calculated. The expres- sions for the variances of incomes of QS was obtained. The obtained results can be used in modeling income changes in various CSN, the virus penetration into it, and also to load control in CSN.

References

[1] Gelenbe E., G-networks with triggered customer movement, Journal of Applied Probability 1993, 30, 742-748.

[2] Matalytski M., Naumenko V., Investigation of G-network with signals at transient behavior, Journal of Applied Mathematics and Computational Mechanics 2014, 13(1), 75-86.

[3] Naumenko V., Matalytski M., Finding the expected incomes in the Markov G-network with signals, Vestnik of GrSU. A Series of Mathematics, Physics, Computer Science, Computer Facilities and Management 2014, 2, 134-143.

[4] Naumenko V., Matalytski M., Investigation and application of G-networks with incomes and signals with random time activation Vestnik of GrSU. A Series of Mathematics, Physics, Computer Science, Computer Facilities and Management 2014, 3, 142-152.

[5] Matalytski M., On some results in analysis and optimization of Markov networks with incomes and their application, Automation and Remote Control 2009, 70(10), 1683-1697.

[6] Naumenko V., Matalytski M., Analysis of Markov net with incomes, positive and negative customers, Informatics 2014, 1, 5-14.